Zinc Creates All Things: SMM Monthly Secondary Zinc Production Launched to Support the Sustainable Blueprint of Zinc Resources

SMM December 25:

In recent years, with the continuous increase in the capacity of zinc ore smelters, the demand for zinc concentrates has risen. However, the growth in zinc concentrate supply has struggled to keep pace, leading to a supply deficit of zinc ore resources. Consequently, processing fees have declined, constraining both raw materials and profits for smelters. Meanwhile, the Government Work Report delivered at the 2025 Two Sessions explicitly called for "strengthening the recycling of waste materials, vigorously promoting the use of secondary materials, and fostering the development of a circular economy." The National Development and Reform Commission (NDRC) and the Ministry of Finance have issued relevant policies and implemented special actions to promote the application of secondary materials. As market attention toward the development of secondary zinc continues to grow, SMM has introduced monthly production data for secondary zinc for market reference.

Throughout the year, production exhibited a pattern of starting low and ending high. The primary reason was that many secondary zinc enterprises had extended Chinese New Year breaks in Q1, leading to relatively low overall production. In Q2, as production resumed after the Chinese New Year holiday, output increased slightly. However, due to rising raw material prices and low zinc ingot prices, profit constraints limited the growth. Entering Q3, the release of new capacity pushed the production center upward, reaching the year’s peak. However, in Q4, profit issues reemerged, resulting in a decline in production.

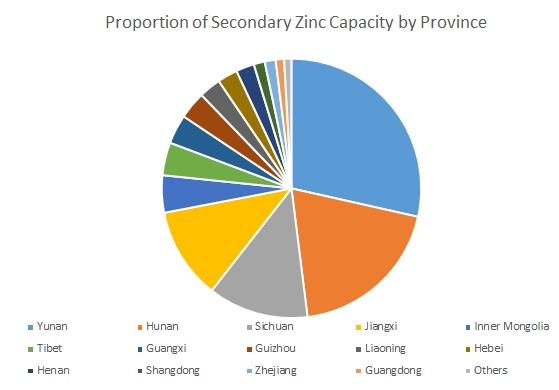

From the perspective of the secondary zinc market distribution, China's secondary zinc capacity is highly concentrated, primarily in regions such as Yunnan, Hunan, and Sichuan. These three provinces account for nearly 60% of the national capacity. However, as raw material issues have intensified in recent years, new secondary zinc capacity has been extending toward northern markets.

What is the current status of each segment in the secondary zinc market, and can production increase in the future?

From the perspective of raw materials for secondary zinc, the primary sources are blast furnace gas ash and electric furnace dust from steel mills. Based on current operating conditions, due to the phase-out of outdated capacity and environmental protection-related controls in steel mills, operations are at a low level compared to the same period, leading to an overall tight supply of raw materials. Additionally, supported by strong consumption of zinc sulfate, prices for low-grade zinc oxide and zinc calcine remain high overall, increasing the raw material costs for secondary zinc.

From the consumption perspective of secondary zinc, its usage areas largely align with those of mined zinc. Overall zinc consumption in November declined by more than 4% MoM, primarily dragged down by environmental protection-driven production restrictions and end-use consumption being in the off-season. Overall, with raw material costs remaining high and consumption support insufficient, secondary zinc enterprises faced severe profit compression, leading to an increase in early holiday shutdowns and maintenance. Production in December is expected to continue declining. Considering the frequent holiday closures among regular enterprises in the first quarter of next year, coupled with unresolved issues of raw materials and profitability, secondary zinc output is projected to remain low.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market exchanges, and relying on SMM's internal database model, for reference only and do not constitute decision-making recommendations./metal.com

۱۴۰۴/۱۰/۰۴، ۱۱:۲۴:۰۲ 11